Rising Yields Creating New Opportunities for CRE Preferred Equity

Higher Treasury yields, tighter lending, and market volatility are creating new opportunities for preferred equity investors in commercial real estate.

Higher Treasury yields, tighter lending, and market volatility are creating new opportunities for preferred equity investors in commercial real estate.

Financial markets ended the week with a sharp selloff in both stocks and bonds, driven by renewed technology volatility and a stronger-than-expected U.S. jobs report.

For commercial real estate investors, the key issue is rising Treasury yields.

As yields move higher, senior debt becomes more expensive, lenders become more conservative, and loan proceeds often decline. That creates capital gaps for sponsors who still own quality assets but can no longer achieve the same leverage available in prior market cycles.

This is where preferred equity becomes more relevant.

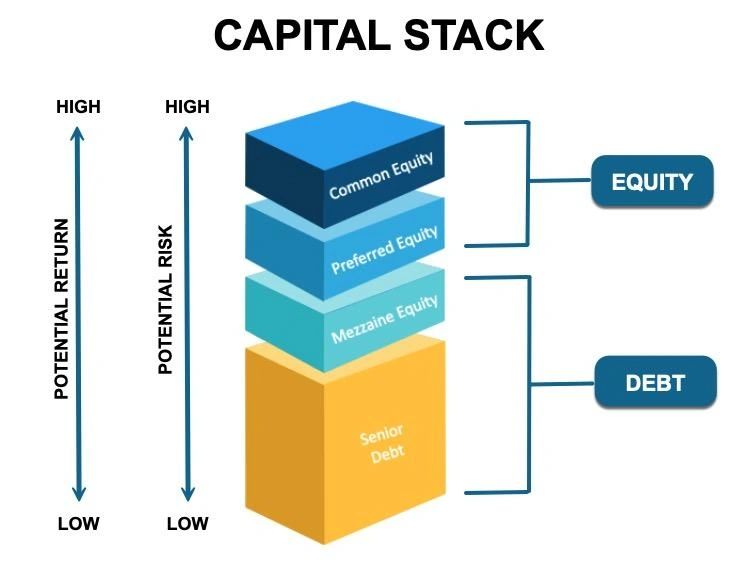

Preferred equity sits between senior debt and common equity in the real estate capital stack. For investors, it can provide a structured position with negotiated priority, defined return targets, and potential downside protections.

For sponsors, it can help bridge the gap between available senior debt and the capital needed to refinance, acquire, complete, or stabilize a property.

The current market is not only about distress. In many cases, the assets may still be fundamentally sound, but the financing environment has changed.

Higher rates, tighter underwriting, private credit pressure, and uncertain inflation have made capital structure more important than ever.

For disciplined preferred equity investors, this volatility can create opportunity.

When senior lenders pull back, structured capital becomes more valuable. The best opportunities are likely to be found in deals with strong sponsorship, realistic valuations, sufficient common equity, a clear business plan, and a credible exit strategy.

As inflation data, Federal Reserve policy, Treasury yields, and private credit liquidity continue to shape the market, preferred equity is likely to remain an important part of commercial real estate finance.

Higher rates are creating challenges for borrowers but for well-structured preferred equity, they may also create attractive investment opportunities.

Markets are risk on. Equity investors need to be risk selective.

Markets are risk-on. Preferred equity investors still need to be risk-selective.

Markets are risk-on. Preferred equity investors still need to be risk-selective.

The past week brought lower oil prices, lower bond yields, and a strong rally in risk assets as markets responded positively to shifting geopolitical headlines.

That is constructive for commercial real estate, but it does not remove the underlying challenges in today’s capital markets.

Many sponsors are still facing:

Higher refinancing costs

Tighter senior loan proceeds

Equity gaps in the capital stack

Slower exits

More conservative valuations

That is where preferred equity can play an important role.

As senior lenders remain disciplined, preferred equity can help sponsors:

Complete acquisitions

Recapitalize existing assets

Fund business plans

Bridge the gap between available debt proceeds and total project costs

But selectivity matters.

In today’s environment, preferred equity investors should remain focused on:

Basis

Downside protection

Sponsorship strength

Durability of NOI

Senior loan structure

Refinance risk

Realistic exit assumptions

Alignment within the capital stack

Public markets may be moving risk-on, but private real estate capital still requires structure, discipline, and protection.

For preferred equity investors, this market is not about chasing yield. It is about identifying the right sponsor, the right basis, and the right structure to create attractive risk-adjusted returns.

Capital is available, but the best opportunities still go to the most disciplined capital.

What does 5% on a 30-Yr Treasury Mean For Real Estate Investors

What does a 5% return on a 30-Year Treasury Mean for Real Estate Investors and Sponsors.

What does a 5% return on a 30-Year Treasury Mean for Real Estate Investors and Sponsors.

The investment market has changed. When the 30-year U.S. Treasury is yielding around 5%, real estate sponsors are no longer competing only against other real estate deals. They are competing against the risk-free rate.

That matters because U.S. Treasuries are considered one of the safest investments in the world. They do not involve leasing risk, construction risk, refinance risk, operating risk, market timing risk, or sponsor execution risk.

So when investors can earn approximately 5% from the U.S. government, private real estate investments must offer a clear reason to take additional risk.

That reason cannot simply be a projected IRR. It has to be a credible, risk-adjusted return.

The Treasury Is Now the Benchmark

In a low-rate environment, investors were often willing to accept lower yields from real estate because the alternatives were limited. If Treasuries were yielding 2% or 3%, a real estate investment offering an 8% preferred return or a mid-teens IRR looked compelling.

Today, the comparison is different. If the risk-free rate is around 5%, then an investor has to ask:

Why should I take private real estate risk for only a modest premium over Treasuries? That question is now central to every capital raise.

Real estate can still offer strong advantages: income, appreciation, tax benefits, inflation protection, and upside from active management. But those benefits have to be weighed against the added risk. The spread has to make sense.

Risk Premiums Matter Again

A higher Treasury yield raises the return hurdle for private investments.

Investors are not just looking at the headline return. They are looking at the premium they are being paid above the risk-free rate.

That means sponsors need to be prepared for tougher questions:

Is the preferred return high enough? Is the current yield strong enough? Is the exit cap rate realistic? Is the debt assumption conservative? Is the business plan achievable? Is the investor adequately protected?

A deal that looked attractive three years ago may not clear the hurdle today. The market is no longer rewarding aggressive assumptions the same way it did in the prior cycle. In this environment, credibility matters more than optimism.

What Investors Are Looking For

Investors are still interested in commercial real estate, but they are being more selective. They want income durability, downside protection, and a clear explanation of why the investment deserves capital in today’s rate environment.

That usually means more focus on:

Strong basis. Conservative leverage. Realistic rent growth. Defensible exit assumptions. Current cash flow. Sponsor co-investment. Preferred equity protections. Clear reporting and control rights.

Investors are also paying closer attention to the capital stack. Common equity may still make sense for certain deals, but many investors are increasingly focused on structured positions that offer priority, defined returns, and better downside protection. That is one reason preferred equity has become more relevant in today’s market.

What Sponsors Need to Do Differently

Sponsors need to recognize that capital is still available, but the bar is higher. The old approach of showing aggressive growth, optimistic exit values, and high projected IRRs is no longer enough. Investors want to see how the deal performs if rates stay elevated, refinancing is more expensive, or exit pricing is less favorable.

Sponsors should adjust by doing four things.

1. Underwrite More Conservatively

Exit cap rates should be realistic. Refinance assumptions should be stress-tested. Rent growth should be supportable. Operating expenses, insurance, taxes, and reserves should not be understated.

Investors will quickly discount projections that appear too aggressive.

The better approach is to show the base case, downside case, and upside case clearly.

2. Emphasize Basis and Downside Protection

In today’s market, basis is one of the most important parts of the story.

A strong acquisition basis, discount to replacement cost, or low leverage point can help investors feel protected even if the market remains uncertain.

Sponsors should clearly explain:

Purchase price versus market value. Cost basis versus replacement cost. Loan-to-cost and loan-to-value. Break-even occupancy. Exit value sensitivity. Investor basis in the capital stack.

A strong basis gives the investment room to breathe.

3. Structure the Deal Around the Investor’s Risk

The structure has to match the market.

If investors are being asked to take more risk than Treasuries, they need to understand how they are being compensated and protected.

That may include a stronger preferred return, current-pay component, maturity date, redemption rights, cash flow sweep, major decision rights, reporting requirements, or other protective provisions.

The goal is not just to offer a higher return. The goal is to offer a better risk-adjusted return.

4. Explain Why the Deal Beats Treasuries

Sponsors should address the Treasury comparison directly.

The investor presentation should answer one simple question:

Why should an investor choose this opportunity over a 5% Treasury?

The answer may include higher current income, appreciation potential, tax benefits, inflation protection, strong collateral coverage, or priority in the capital stack.

But the answer must be clear. If the sponsor cannot explain the risk premium, the investor will struggle to justify the allocation.

The Bottom Line

A 5% 30-year Treasury does not mean investors will stop investing in real estate.

It means real estate deals have to work harder to earn their capital.

Investors now have a stronger risk-free alternative, so sponsors must offer better structure, better underwriting, better downside protection, and a more compelling return premium.

The best sponsors will adapt. They will buy at a stronger basis, use leverage carefully, present conservative assumptions, and structure deals around investor protection.

This is not a bad market for commercial real estate. It is a more disciplined one. And in a disciplined market, the best opportunities are not the ones with the biggest projections.

They are the ones where the risk-adjusted return is clear.

The Bond Market Is Repricing Commercial Real Estate Capital

The Bond Market Is Repricing Commercial Real Estate Capital. The recent global bond market sell-off was more than a Wall Street headline. For commercial real estate, it directly impacts valuations, refinance proceeds, de…

The Bond Market Is Repricing Commercial Real Estate Capital. The recent global bond market sell-off was more than a Wall Street headline. For commercial real estate, it directly impacts valuations, refinance proceeds, debt service coverage, and capital stack structuring.

From a preferred equity investor’s perspective, the key takeaway is simple:

Higher-for-longer rates may be the new underwriting environment.

That matters because many CRE deals were capitalized when debt was cheaper, refinance assumptions were easier to support, and cap rates were more forgiving. Today, higher rates are changing the math.

When debt becomes more expensive:

➡️ Senior loan proceeds may be reduced ➡️ DSCR constraints become more important ➡️ Debt yield may drive sizing more than LTV ➡️ Refinances may not fully repay existing debt ➡️ Reserves, rate caps, and carry costs become more expensive ➡️ Exit cap rates need to be more conservative

For many sponsors, this creates a financing gap.

For preferred equity investors, it creates both risk and opportunity.

A property may still be fundamentally sound. The occupancy may be stable. The sponsor may have a credible business plan. The market may still support long-term value.

But if the current capital stack was built for a lower-rate environment, the refinance may not work.

That is where preferred equity can become relevant.

Preferred equity can help bridge the gap between senior debt and common equity. It can allow a sponsor to complete a business plan, preserve ownership, avoid a forced sale, or stabilize an asset through a more difficult financing environment.

But the structure matters.

Preferred equity should be underwritten around downside protection, not just projected returns. Investors should be focused on basis, cash flow, senior debt terms, reserves, sponsor alignment, control rights, and exit risk.

The most important question is no longer simply:

“What is the property worth?”

The better question is:

“How much capital can the property actually support in today’s market?”

That is where many CRE owners may feel the reset.

The capital is still available, but it is more selective. Deals need more realistic leverage, stronger reserves, conservative exits, and clearer alignment between sponsor and investor.

For sponsors, preparation matters.

For preferred equity investors, discipline matters.

The CRE Market Is Entering an Execution-Driven Cycle

The CRE Market Is Entering an Execution-Driven Cycle. Why Preferred Equity Is Becoming Increasingly Important.

The CRE Market Is Entering an Execution-Driven Cycle. Why Preferred Equity Is Becoming Increasingly Important.

Commercial real estate is transitioning into a fundamentally different operating environment.

Persistent inflation, geopolitical instability, elevated interest rates, supply-chain disruptions, and tightening credit conditions are reshaping how real estate transactions are capitalized, underwritten, and executed across the market.

While public equity markets continue pushing toward record highs, the underlying realities facing commercial real estate owners and operators are becoming increasingly complex.

At CRE Equity, we believe the market is moving away from a liquidity-driven cycle and into an execution-driven cycle — one where disciplined capitalization, operational expertise, and structured finance solutions will determine which sponsors outperform.

Why This Matters for Commercial Real Estate

Several macroeconomic themes are directly impacting commercial real estate finance today:

Higher-for-Longer Interest Rates

With Treasury yields remaining elevated and central banks continuing to combat inflation, refinancing risk has become one of the defining issues across CRE.

Traditional senior lenders remain conservative, leverage levels have compressed, and many projects are facing capital gaps between existing debt proceeds and total capitalization requirements.

This environment is increasing demand for flexible structured capital solutions.

Construction and Operating Cost Pressure

Global supply disruptions and energy volatility continue affecting construction materials, transportation, labor, and operating expenses.

For development and transitional assets, execution risk has become materially more important than during the low-rate environment of prior years.

Sponsors with insufficient liquidity, weak contingency planning, or overleveraged capital stacks may face increasing pressure moving forward.

Capital Markets Dispersion

One of the defining characteristics of this cycle is likely to be widening dispersion between winners and losers.

Assets with strong sponsorship, durable cash flow, conservative leverage, and operational expertise may continue to perform well, while weaker projects could face refinancing challenges, recapitalizations, or distress.

This creates both risk and opportunity across the market.

The Growing Role of Preferred Equity

In today’s environment, preferred equity is becoming an increasingly important component of commercial real estate capitalization strategies.

Preferred equity can provide:

• Supplemental capital to close leverage gaps • Rescue capital for refinancing or maturity events • Structured liquidity solutions for sponsors • Flexible capitalization for transitional or lease-up assets • Reduced dilution versus common equity alternatives • Alignment between institutional capital and experienced operators

As traditional lending markets remain constrained, many sponsors are seeking institutional preferred equity solutions that provide both flexibility and certainty of execution.

Our Perspective

At CRE Equity, we believe the next 12 to 24 months may present some of the most compelling risk-adjusted opportunities the market has seen in years particularly for disciplined sponsors with strong operational capabilities and properly structured capitalization.

The market is no longer rewarding aggressive leverage or speculative appreciation assumptions. It is rewarding execution.

Sponsors who can navigate construction costs, manage liquidity, protect debt service coverage, and structure resilient capital stacks will be positioned to capitalize on the opportunities emerging in this cycle.

In periods of market dislocation, capital structure matters more than ever.

Preferred Equity and Structured CRE Finance in 2026:

Preferred Equity and Structured CRE Finance in 2026: How Sponsors Are Closing the Capital Gap.

Preferred Equity and Structured CRE Finance in 2026: How Sponsors Are Closing the Capital Gap.

As refinancing pressure builds across commercial real estate, sponsors are turning to preferred equity and structured finance solutions to bridge capital gaps and complete transactions.

Commercial real estate capital markets are entering a new phase in 2026, one defined less by liquidity constraints and more by capital structure complexity.

While debt markets have shown modest improvement in recent months, the reality for many sponsors is that traditional financing alone is no longer sufficient to execute acquisitions, refinances, or recapitalizations. As loan proceeds remain constrained and underwriting standards stay disciplined, a growing number of transactions are requiring layered capital solutions to move forward.

The Growing Capital Gap in CRE Transactions

Across multiple asset classes, a consistent trend has emerged. There is a widening gap between senior loan proceeds and total capital required.

Several factors are driving this dynamic. Elevated interest rates continue to impact debt service coverage. Lenders remain conservative on loan-to-value and debt yield. Operating expenses have increased across many asset classes, particularly in multifamily and office. Transitional business plans also require additional reserves and flexibility.

Even with improving loan spreads, many deals today are underwriting to lower leverage levels, forcing sponsors to either contribute more equity or seek alternative capital sources.

Why Preferred Equity Is Gaining Momentum

In this environment, preferred equity and structured finance solutions are becoming a critical part of the capital stack.

Preferred equity is increasingly being utilized to bridge the gap between senior debt and sponsor equity, enhance returns without fully diluting ownership through joint venture structures, provide flexibility in transitional business plans, and facilitate recapitalizations where existing debt cannot be fully refinanced.

Unlike traditional joint venture equity, preferred equity allows sponsors to retain greater control while still accessing the capital needed to execute their strategy.

At the same time, investors are attracted to preferred equity for its risk-adjusted return profile, typically positioned between senior debt and common equity in the capital stack.

A More Structured Approach to Deal Execution

Transactions in today’s market are no longer driven solely by leverage. They are driven by structure.

Sponsors are increasingly evaluating combinations of senior debt and preferred equity financing alongside bridge loans, and hybrid capital structures tailored to lease-up or repositioning strategies. Recapitalizations are also becoming more common as a way to reset the capital stack without requiring a full exit.

This shift reflects a broader evolution in the market, where capital partners are selected as much for their flexibility as for their pricing.

Where Opportunities Are Emerging

Despite ongoing challenges in certain sectors, capital continues to flow toward multifamily assets with stable or improving fundamentals, industrial and logistics properties with strong demand drivers, and select hospitality and niche asset classes with clear repositioning upside.

Office assets, while still facing structural headwinds, are also creating opportunistic entry points. These situations often require more creative capital structures to align risk and return expectations.

Looking Ahead

As the commercial real estate market continues to adjust, the ability to structure capital effectively will remain a key differentiator.

Sponsors who proactively address capital gaps, align with the right equity partners, and approach transactions with flexibility are better positioned to execute in today’s environment.

Preferred equity and structured capital solutions are becoming core tools in modern real estate finance. Understanding how to navigate the capital stack is essential to unlocking opportunities in 2026 and beyond.

The Commercial Real Estate Market Reset Is Here – What Deep Office Discounts Mean for Investors.

The Commercial Real Estate Market Reset Is Here – What Deep Office Discounts Mean for Investors.

The U.S. commercial real estate market is going through a major reset, and for those paying attention, it is creating some of the most compelling opportunities in years.

Office assets are repricing aggressively

After holding out for a recovery following the pandemic, many office owners and lenders are now accepting a different reality. Demand has shifted as hybrid work becomes permanent, and interest rates remain elevated.

As a result, a wave of distressed sales has hit the market, with some properties trading at discounts of 90 percent or more from prior values.

In 2025, more than five billion dollars in distressed office properties were sold through foreclosures, auctions, and lender driven sales.

This is not just a correction. It is a full reset of the office sector.

Why this matters

These pricing declines are not only losses for existing owners. They are also entry points for new investors.

Across the market, several trends are emerging. Investors are acquiring assets at significant discounts to replacement cost. There is growing interest in converting office buildings into residential or mixed use properties. Operators are exploring creative repositioning strategies for obsolete buildings. Lenders are becoming more flexible as they work through distressed situations.

For experienced sponsors, this is where long term value is created.

Not all sectors are moving in the same direction

While office is under pressure, other areas of commercial real estate are showing different dynamics.

In certain housing markets, competition remains intense. In the Hartford, Connecticut area, buyers are still entering bidding wars, often making offers above asking price and waiving inspections. Home values there have risen substantially over the past several years.

In the multifamily sector, a large share of properties are offering rent concessions. This is largely driven by an oversupply of new units in high growth regions that saw heavy construction during the pandemic.

Industrial real estate is also seeing some normalization. Vacancy rates have increased in certain markets as logistics demand adjusts, although fundamentals remain stronger than office.

Capital is still active but more selective

Even with these challenges, capital has not disappeared. It has simply become more disciplined and more selective.

Large scale investments are still happening, particularly in areas tied to long term economic growth. Cities are continuing to invest in infrastructure and development that can drive tourism and business activity.

The broader trend is clear. Capital is moving toward opportunities with strong fundamentals and clear long term demand.

What investors should be watching

As the market continues to adjust, success will depend on strategy and execution.

Investors should be paying close attention to distressed office acquisitions and note sales, opportunities to convert or reposition existing assets, and situations where recapitalization or restructuring can unlock value.

Markets with strong population and job growth will continue to attract capital. At the same time, some assets are being mispriced due to short term liquidity pressures, creating opportunities for those prepared to act.

Bottom line

This is not the end of commercial real estate. It is a transition.

The gap between strong and weak assets is widening, and the next phase of the market will reward those who can identify opportunity early and execute effectively.

For investors who understand the cycle, this environment may offer some of the best opportunities in the coming years.

Last week was a strong one for markets, with equities pushing to new highs and momentum continuing.

Last week was a strong one for markets, with equities pushing to new highs and momentum continuing.

At the same time, global policymakers are flagging a more complex backdrop, with slower growth and lingering inflation pressures.

So what’s really going on?

We’re seeing a market that is:

• holding up better than expected, especially in the U.S. • supported by continued confidence in capital markets and deal flow • navigating real but manageable macro and geopolitical risks

What this means for commercial real estate: Deals are still getting done. Capital is still moving.

But the environment is rewarding thoughtful underwriting, strong sponsorship, and clear execution.

The bigger picture: There’s a growing gap between headlines and reality.

And right now, the reality is this: the market is more resilient than many expected, but still evolving.

Deploying Preferred Equity in Today’s Commercial Real Estate Market | CRE-Equity.com

Deploying Preferred Equity in Today’s Commercial Real Estate Market | CRE-Equity.com

The commercial real estate market is in a transitional phase, and that shift is creating opportunity.

Higher interest rates and tighter lending standards have reduced leverage across the board, leaving many strong deals with gaps in the capital stack. As a result, demand for preferred equity in commercial real estate continues to grow.

Filling the Capital Gap

Sponsors are increasingly turning to preferred equity investments to bridge the space between senior debt and common equity. Whether for acquisitions, refinances, or transitional assets, preferred equity is helping move deals forward.

We are seeing this most often in:

Multifamily recapitalizations

Value-add and lease-up projects

Bridge-to-stabilization scenarios

Why Pref Equity Is Gaining Momentum

For sponsors, preferred equity for real estate deals offers preservation of ownership, flexible structuring, and efficient execution.

For investors, it provides priority in the capital stack, attractive risk-adjusted returns, and downside protection relative to common equity.

Our Focus at CRE-Equity.com

We are actively sourcing and placing preferred equity investments from $250,000 to $2.5 million across commercial real estate opportunities nationwide.

Our focus remains on experienced sponsors, clear business plans, and assets positioned for stabilization or growth.

Final Thought

As lending remains constrained, preferred equity in commercial real estate is becoming a key component of how deals get done.

For sponsors and investors alike, today’s market presents a compelling opportunity to deploy capital with structure and discipline.